Home Insurance Guide: What Does It Cover?

Did you know that about 80% of U.S. homeowners don’t realize how much their stuff is worth? This can lead to a big gap in their home insurance. Knowing what home insurance covers is key to protecting your investment and making sure you’re safe from unexpected events. Home insurance is more than just a rule; it’s a vital financial shield that can prevent big losses. This guide will walk you through home insurance coverage. We’ll explore the benefits of a strong home insurance policy. And we’ll cover the important things every homeowner should know. Key Takeaways What does home insurance cover includes protection for the structure and contents of your home. Home insurance coverage can serve as a critical financial safety net in times of disaster. Understanding home insurance policy benefits helps ensure you obtain adequate coverage. Many mortgage lenders require proof of home insurance during the home buying process. Misestimating the value of your possessions can result in insufficient coverage. Understanding Homeowners Insurance Homeowners insurance is key to protecting our biggest investments. It covers financial losses related to our homes. Knowing how important it is helps us make smart choices. This way, we can avoid financial harm from unexpected events. Let’s explore what homeowners insurance includes. We’ll look at important terms and how to understand claims. This will help us grasp our policy details better. Definition and Importance Homeowners insurance protects our homes and personal items from risks like theft and fire. It’s vital for our financial safety. It helps cover repair or replacement costs from unexpected events. Every homeowner should understand this. A good insurance policy acts as a safety net. It keeps our assets and resources safe. Key Terms to Know Premium: The amount paid for the insurance policy, usually on a monthly or annual basis. Deductible: The out-of-pocket expense that must be paid before the insurance coverage applies in the event of a claim. Replacement Cost: The amount it would take to replace damaged property with similar new items, without deducting for depreciation. Liability Coverage: A component of the policy that protects against legal claims for injury or damage to others while on your property. Actual Cash Value: The cost to replace property minus depreciation, which may differ from replacement costs. What Does Home Insurance Cover? It’s important for homeowners to understand what their home insurance covers. Home insurance usually includes several types of coverage to protect against different risks. Knowing these categories helps us see the benefits of having the right coverage. Many things can affect what your home insurance covers. These factors can change the scope and limits of the protection. Standard Types of Coverage A typical home insurance policy has several key parts: Dwelling Coverage: This part protects the structure of our home from damage, giving us peace of mind. Personal Property Coverage: It covers our belongings inside the home, protecting our personal items from loss. Liability Coverage: This part helps with legal costs if someone sues us, covering expenses. Common Events Covered by Policies Home insurance policies often cover many common events. These include: Fire and smoke damage Theft or vandalism Weather-related incidents like windstorms and hail damage Liability for injuries on our property Dwelling Coverage and Its Importance Dwelling coverage is key in home insurance. It protects the physical part of our home. This includes walls, roofs, floors, and built-in appliances. It ensures our living space is safe from various risks. Knowing about dwelling coverage helps us understand our insurance needs better. It gives us peace of mind when damage happens. What Does Dwelling Coverage Include? This coverage usually covers: Damage from risks like fire, wind, or hail. Repairs for built-in appliances and systems, such as heating or plumbing. Coverage for extra structures like garages or decks. Coverage Limits for Dwelling It’s important to know about home insurance coverage limits. These limits show the most the insurance will pay for repairs or rebuilds after a loss. Several things affect these limits: The current market value of the home. The cost of local materials and labor. The size and features of the home. Choosing the right dwelling coverage means valuing our property right. It also means thinking about possible repair costs. Knowing about these limits helps protect our finances when unexpected things happen. Personal Property Coverage Explained It’s key to know about personal property coverage in a home insurance policy. This part helps protect our valuable stuff from theft, fire, or vandalism. By understanding what’s covered, we can choose the right insurance for our needs. What Personal Belongings Are Covered? Home insurance policies usually list what personal property they cover. They protect many items, like: Furniture and furnishings Electronics such as TVs and computers Clothing and personal accessories Jewelry, artwork, and collectibles (usually with specific limits) It’s important to check the policy for limits on expensive items. This helps us decide if we need extra coverage. For more details, look at the full home insurance policy details. Coverage While Off-Premises Many people don’t know that personal property coverage goes beyond their homes. Insurance can apply when items are taken elsewhere. Valuables like laptops and cameras might be covered while traveling. But, there are often limits, so it’s good to know what’s covered inside and outside the home. Liability Coverage: Protecting Your Finances Liability coverage is key for homeowners to protect their finances. It helps cover damages or injuries caused by household members to others or their property. Without it, unexpected events can lead to big expenses. What Liability Coverage Entails Liability coverage in home insurance policies includes several important parts: Medical expenses for injuries on our property Legal fees for defending against lawsuits Costs for repairing damages to others’ belongings Coverage limits that differ by policy Why Liability Coverage is Crucial This coverage is vital for financial protection. It helps avoid lawsuits and financial stress from accidents. It gives families peace of mind and security. Type of Coverage Description Typical Coverage Limits Medical Payments Covers minor injuries on your property $1,000

Why Life Insurance Reflects Love, Not Fear

Did you know about 60% of Americans don’t have life insurance? They often worry about the cost and how complicated it is. But, life insurance is really about showing love for our families. It’s not about fear, but about making sure they’re financially secure. Life insurance is like a safety net for our loved ones. It lets them keep living their lives even when we’re not there. It shows how much we care about their future. By getting life insurance, we’re putting our family first, showing we’re all in this together. Key Takeaways Life insurance is an expression of love and commitment to your family’s financial security. Understanding the importance of life insurance helps dispel misconceptions related to fear. Investing in life insurance provides long-term support for loved ones. Policyholders contribute to their family’s stability and peace of mind. Prioritizing family protection is a key motivation for purchasing life insurance. Understanding the True Purpose of Life Insurance Life insurance is more than just a policy. It shows our love and care for our families. It helps protect them from financial stress when we’re not there. What Life Insurance Means for Your Loved Ones Life insurance gives our families a solid base. It helps them manage costs like mortgages and school fees. This lets them live without worrying about money. It’s a big help during tough times. It lets families focus on healing, not just surviving. The Emotional Impact of Coverage Having life insurance brings peace of mind. It makes families feel safer and more supported. It turns hard times into moments of love and support. Life insurance shows our love and care for our families. It balances their emotional and financial needs. It’s a true sign of our dedication to them. Why Life Insurance Is About Love, Not Fear Life insurance is more than just a financial plan. It shows our deep love and care for those close to us. By getting life insurance, we tell our loved ones we care about their future. This choice helps them now and secures their future success. Life Insurance and the Message of Care Life insurance is about love, not fear. It sends a strong message of care. When we get a policy, we protect our loved ones’ future. This shows our commitment to their well-being and prepares them for the unexpected. Building a Legacy Through Financial Security Life insurance brings financial security, which is key to building a legacy. It helps future generations achieve their dreams without financial worries. By choosing this option, we make a lasting difference in their lives. For more information, check out how life insurance can help build a legacy. Life Insurance Benefits Beyond Financial Planning Life insurance does more than just help with money planning. It brings a mix of comfort and support to families in tough times. This helps families feel secure, knowing they have the support they need when it counts most. Peace of Mind for Families Life insurance offers a lot of comfort in uncertain times. It ensures bills get paid, kids get an education, and daily needs are met. This lets families heal and move forward without worrying about money. Creating Generational Wealth and Stability Life insurance is also key in building wealth for generations to come. It’s not just about a safety net; it’s about investing in the future. This way, we ensure our family’s financial security and legacy for years to come. It shows life insurance is more than a policy; it’s a dream for our family’s future. Opening Up Conversations About Family Protection Talking about life insurance is key to securing our loved ones’ futures. Choosing the right time for these talks is important. Holidays are great for this because they bring us together and make talking about money easier. By discussing life insurance during holidays, we make it clearer why it’s important. It shows we care for each other’s well-being. Why Holidays are Ideal for Discussing Financial Matters Holiday gatherings are perfect for these talks. They offer a warm setting for discussing sensitive topics. Here’s why: Everyone is together in a comfortable environment. Shared values and concerns can facilitate understanding. Opportunities for storytelling to illustrate experiences with family protection. Tips for Productive Family Discussions To have effective talks about life insurance, we need to be thoughtful. Here are some tips: Be open and honest: Share your thoughts and concerns candidly. Listen actively: Encourage family members to express their views and feelings. Align on objectives: Discuss goals for family protection to ensure everyone is on the same page. Be supportive: Acknowledge that these discussions can be challenging but are necessary for peace of mind. By following these tips, we can have meaningful talks about family protection. This helps everyone understand the value of life insurance. It’s a step towards a secure future for our families. Conclusion Life insurance is all about love, not fear. It’s a way to protect our families and ensure their financial security. It gives us peace of mind, knowing they are safe. Getting life insurance shows our love in a real way. It helps avoid financial worries and adds to our emotional support. It prepares our families for life’s ups and downs. Talking about life insurance helps us understand and care for each other more. Let’s see planning for our loved ones as a way to strengthen our bonds. It prepares us for a secure future together. FAQ What are the primary benefits of life insurance? Life insurance offers key benefits like protecting your family, securing their finances, and giving you peace of mind. It helps ensure your loved ones can keep their lifestyle and pay for important expenses after you’re gone. How does life insurance provide peace of mind? Life insurance gives you peace of mind by protecting your family’s finances. It means they’ll have the money they need to cover daily costs when times are tough. Can life insurance be seen as a way to build a legacy? Yes, life insurance can help

Life Insurance for Business Owners: A Guide.

Did you know about 70% of small business owners lack life insurance? This fact shows a big gap in planning among entrepreneurs. It leaves their families and businesses at risk of sudden events. In this guide, we’ll talk about why life insurance is key for business owners. It helps secure your future and keep your business legacy alive. Life insurance for business owners is more than just a policy. It’s a vital part of your financial plan that brings peace of mind. We’ll look at different life insurance options for self-employed people. We’ll show how these can fit your specific needs. Our goal is to make life insurance for business owners clear and explain its role in protecting your family and business. We’ll dive into the different policies and how they work. We’ll highlight life insurance’s role in reducing financial risks of owning a business. Being prepared helps keep your company strong and stable for the future. Start your search for the right coverage by checking out insurance quotes made for you. Key Takeaways Understanding life insurance’s role in protecting your business and family. Exploring various life insurance options available for business owners. Evaluating the ownership structures of life insurance policies. Recognizing the financial risks inherent in business ownership. Gaining insights into retirement planning features of life insurance. Understanding the Importance of Life Insurance for Business Owners Being a business owner comes with many challenges, including financial risks. We must be ready for unexpected events, like losing a key team member. These events can harm our business and personal lives. Life insurance helps by providing a financial safety net, keeping our business stable and protecting our families. The Financial Risks of Business Ownership Business owners face many risks that can hurt their finances. Market changes, operational issues, and personal events can all be tough. Without a plan, losing a key team member can cause financial trouble. Life insurance helps by protecting our businesses from these risks. Protecting Your Business and Family Keeping our business and family safe is key. Life insurance gives us financial security. It helps manage debts, keeps operations running, and supports our loved ones. This way, we can focus on growing our business without worrying about unexpected problems. Continuity Planning and Succession Good business planning is essential for entrepreneurs. Life insurance supports succession plans, helping our businesses smoothly change hands. It ensures our legacy is protected and sets the stage for our business’s future success, even when we’re not there. Types of Life Insurance Policies Available Business owners have many life insurance options. It’s key to know the different types to match coverage with business goals. Each type meets unique financial needs, giving flexibility in protection and planning. Term Life Insurance Term life insurance covers you for a set time, from one to thirty years. It’s a top pick for entrepreneurs wanting simple, affordable coverage. The premiums are lower than permanent options, making it great for startups with short-term financial needs. Whole Life Insurance Whole life insurance covers you for life if you keep paying premiums. It also grows a cash value over time. This makes it good for building wealth and securing legacies, alongside small business life insurance. Universal Life Insurance Universal life insurance lets you adjust premiums and invest cash value. It’s good for those who like market changes, giving more control over cash value growth. It’s a solid choice for entrepreneurs looking at their financial needs and risk levels. Life Insurance for Business Owners: Ownership Considerations Choosing the right ownership structure for life insurance is key. It can greatly affect your business’s finances. Knowing the difference between personal and corporate-owned life insurance helps align your choices with your business goals. Personal vs. Corporate Ownership Personal life insurance is held by an individual. It mainly supports personal financial planning and estate planning. On the other hand, corporate-owned life insurance is held by the company. It offers several benefits for the business. Your choice should match your business strategy. It should aim to maximize value. Advantages of Corporate-Owned Policies Corporate-owned life insurance can improve a business’s liquidity. It keeps funds for operations or transitions. It also supports share purchases during ownership changes, keeping control. It also has tax benefits, like using a Capital Dividend Account (CDA) for tax-free payments. This makes it appealing for long-term growth. Potential Risks and Disadvantages Corporate-owned life insurance has its downsides. It can bring complexities in compliance and regulatory issues. It requires careful management. Personal life insurance ownership might be simpler for estate planning. It’s important to weigh these options carefully. This ensures your choice aligns with your future goals. Understanding ownership considerations is key. It helps you choose the best option for your business and financial goals. The Role of Life Insurance in Business Owner Retirement Planning Life insurance is key for business owners planning for retirement. It offers death benefits and helps build cash value. This makes it a great tool for financial security in retirement. Building Cash Value Permanent life insurance lets you build cash value over time. This money grows tax-free, ready for use in retirement. It’s perfect for covering unexpected costs or new investment chances. Supplementing Retirement Income Using life insurance in retirement planning adds a unique twist. It lets you tap into cash value for extra income. This boosts your financial security in retirement. Tax Advantages of Corporate-Owned Life Insurance Corporate-owned life insurance offers big tax benefits. It grows cash value without taxes and may give tax-free dividends. These perks help lower taxes and improve your financial future. Choosing the Best Life Insurance for Entrepreneurs Choosing the right life insurance is key for entrepreneurs to protect their businesses and families. It’s important to understand their unique needs. This helps make better choices about coverage. Assessing Your Business Needs Understanding your business’s specific needs is vital. Consider things like: Outstanding debts Revenue replacement Succession planning These factors help figure out how much coverage you need. It ensures your business and family are safe in tough

How Life Insurance Supports Loved Ones After Loss.

Did you know nearly 40% of Americans don’t have life insurance? This shows a big gap in financial protection. It could leave families at risk during tough times. Knowing how life insurance helps loved ones after loss is key to keeping families safe and supporting them in grief. Life insurance benefits can be a vital financial safety net. They cover things like mortgages, education, and daily living costs. In this article, we’ll look at why life insurance is important. We’ll see how it can protect our loved ones when they need it most. Key Takeaways Life insurance serves as a vital financial safety net for families. It provides peace of mind regarding future financial protection. Understanding different life insurance policies is key to effective planning. Death benefits can address various financial obligations after a loss. Properly naming beneficiaries ensures effective distribution of benefits. Understanding Life Insurance and Its Importance Life insurance is key to financial planning. It helps manage risks from life’s unknowns. Knowing about life insurance lets us protect our families financially. Definition of Life Insurance Life insurance is a deal between you and an insurance company. They promise to pay a set amount to your loved ones when you pass away. This helps ease financial worries for those left behind. Types of Life Insurance Policies There are many life insurance options. Here are the main ones: Type of Policy Features Life Insurance Benefits Term Life Insurance Provides coverage for a specific period, usually 10 to 30 years. Lower premiums; benefits paid if death occurs during the term. Whole Life Insurance Offers lifelong coverage with fixed premiums and a cash value component. Guaranteed death benefit; cash value can grow over time. Universal Life Insurance Flexible premiums and death benefits; can accumulate cash value. Adjustable coverage; use cash value for premiums. How Life Insurance Provides Financial Protection Life insurance is a vital financial tool. It helps your family avoid financial stress when you’re gone. It covers education, mortgages, and daily needs. This way, your family can heal without worrying about money. How Life Insurance Supports Loved Ones After Loss Life insurance is key in helping families financially during tough times. It ensures loved ones get the support they need to face both immediate and long-term financial hurdles after losing a family member. Knowing how these benefits work helps keep families secure. The Role of Death Benefits Death benefits from life insurance policies help by covering various costs during hard times. These include: Funeral and burial costs Paying off outstanding debts Replacing lost income for dependents These funds help families manage some of the financial stress that comes with loss. This shows how vital death benefits are. Who Can Be Named as Beneficiaries Life insurance policies let policyholders choose who gets the death benefits. Common choices are: Spouse Children Parents Other family members or trusted individuals Choosing beneficiaries clearly means the funds go where the policyholder wants. This brings peace of mind and strengthens family security when needed most. Common Uses for Death Benefits Death benefits are used in many ways to help families. They can be used for: Paying for daily living expenses Funding education for children Contributing to retirement savings Settling debts such as mortgages or credit cards Understanding these uses helps families plan better for the future. We suggest everyone look into life insurance and learn more from reliable sources. The Process of Claiming Death Benefits Claiming death benefits can be tough during a time of loss. Knowing the steps can help. First, the beneficiary or executor must contact the insurance company. They need to submit a claim with the right documents. Submitting a Claim To start, the beneficiary should contact the insurance company. It’s good to have policy details and identification ready. Each company has its own rules, so check theirs to make things easier. Documents Needed for Claim Processing Having the right documents is key for a smooth claim. You’ll need: Death certificate Policy details Identification of the claimant Any forms the insurance company asks for Having these documents ready can make the process easier. Typical Timelines for Benefit Payout Knowing how long it takes to get benefits is important. It can be a few weeks to several months. The time depends on the case’s complexity and the documents you provide. Keep in touch with the insurance company to know how your claim is doing. Step Description Estimated Timeframe Contact Insurance Start the claim by contacting the insurance company. Immediate Gather Documents Get all the documents needed for the claim. 1-2 weeks Submit Claim Send in the claim with all documents. Immediate upon completion Claim Review The insurance company checks the claim. 2-6 weeks Benefit Payout The insurance pays out the benefits. 1-3 weeks Ensuring Family Security with Life Insurance Life insurance is key to keeping families safe. It offers a financial safety net that reassures us and our loved ones. Knowing our families are protected gives us confidence to face life’s unknowns. Understanding how life insurance fits into estate planning helps us prepare better. The Peace of Mind That Comes with Coverage Life insurance lets us focus on our families’ well-being without financial worries. It ensures funds for immediate needs, medical bills, and daily living costs. This peace of mind is invaluable. We can focus on healing and emotional recovery, knowing our families are financially secure. How Life Insurance Fits into Estate Planning Adding life insurance to our estate plans is vital for financial protection. It helps ensure our wishes are followed, supporting family security. Life insurance can cover estate taxes, letting heirs inherit without financial stress. By including life insurance in our estate plans, we ensure long-term stability for our loved ones. Addressing Common Concerns and Misconceptions It’s important to understand life insurance misconceptions. Many think it’s only for those with dependents. But it offers financial resources for funeral costs, debts, or future needs. We must clear up these misconceptions to ensure we have the right coverage for our families. Concern/Misconception Reality Life

Best Time to Buy Life Insurance: Key Tips.

Did you know nearly 60% of Americans don’t have life insurance? This fact shows how vital it is to know when to buy life insurance. It’s not just about money; it’s about protecting our loved ones and securing our financial future. We’ll dive into the best times to buy life insurance and share tips to guide you. By the end, you’ll see how life insurance is a shield and a smart investment for your peace of mind. Key Takeaways Understanding when is the best time to buy life insurance can enhance financial security. Life insurance provides essential financial support for loved ones after a loss. Timing the purchase of life insurance can impact costs and coverage options. Key life milestones often trigger the need for life insurance. Evaluating personal circumstances is key for making the right choices. Comparing policy options ensures smart consumer decisions. Understanding the Importance of Life Insurance Life insurance is key to securing our families’ financial futures. It offers vital support during tough times. It’s essential when family members depend on one income to live comfortably. Financial Protection for Loved Ones Our loved ones’ financial security is a top priority. Life insurance covers living costs, education, and final arrangements. It ensures our family’s well-being, giving us peace of mind. Coverage for Major Debts Life insurance also helps with major debts. Debts like mortgages or loans can be overwhelming. It helps keep our family’s finances stable, easing stress during hard times. Investment in Peace of Mind Life insurance is an investment in peace of mind. It lets us know our families are set, no matter what. It’s a smart move for financial security and planning. Factors to Consider When Buying Life Insurance When you’re looking at life insurance, it’s important to think about a few key things. Your age and health are big factors in how much you’ll pay and if you can get coverage. Also, think about your financial needs and what your family depends on you for. Choosing a policy that fits your long-term goals is also key. This way, your life insurance does more than just cover immediate needs. It also helps you reach your future dreams. Your Age and Health Status Your age and health really matter when it comes to life insurance. Young people usually pay less because they’re healthier. Knowing your health status helps when you apply for insurance. Financial Obligations and Dependents It’s important to know what you owe and who depends on you. This includes debts, mortgages, and family needs. This ensures your loved ones are taken care of if something unexpected happens. Long-Term Financial Goals Think about your future financial plans when choosing life insurance. It should support your retirement or estate planning goals. At the same time, it should also give you peace of mind today. When Is the Best Time to Buy Life Insurance? Knowing when to buy life insurance is key to getting the most out of it. We look at the best age to buy, how big life events affect your needs, and the dangers of waiting too long. Optimal Age for Purchasing Life Insurance The best time to buy life insurance is usually between the mid-20s and early 30s. At this age, you likely have fewer responsibilities and better health. This means you can get lower premiums. Buying insurance at this age also saves you money in the long run. It ensures your family is protected early on. Timing Around Major Life Events Big life events like getting married, having kids, or buying a home are key times to think about life insurance. These events add new financial duties. They make it important to check if your insurance needs have changed. Using a life insurance timing guide during these times is smart. It helps keep your finances secure for the future. Waiting Risks and Cost Implications Delaying life insurance purchase can lead to higher costs. Rates can go up by 4-8% each year for people aged 25-45. Waiting means paying more and might even mean you can’t get coverage later. Buying insurance early gives you peace of mind. It also helps secure your family’s financial future. Age Range Typical Premium Increase per Year Financial Responsibility Mid-20s to Early 30s Baseline Minimal Mid-30s to Early 40s 4-8% Increasing Late 40s and Beyond Significantly Higher Maximal Term life insurance is a good choice for those wanting affordable coverage. It offers a big death benefit for a set time. This fits both your needs and budget. For more on insurance options, check out this informative source. Key Life Milestones to Trigger Life Insurance Purchase Some life events are key times to think about getting life insurance. These moments help protect you, your family, and your financial goals. Getting Married or Starting a Family Getting married or starting a family brings new financial duties. Life insurance is key to safeguarding your loved ones. It ensures they’re cared for, even if you’re not there. Buying a Home Buying a home means taking on a big mortgage. Life insurance can help cover this debt. It keeps your family’s living standards high, even in tough times. Starting a Business Starting a business comes with risks. Business insurance helps manage these risks. Life insurance also plays a big role, like in buy-sell agreements. It keeps your business running smoothly. Preparing for Retirement As you near retirement, check your life insurance needs. It might be time to adjust your coverage. This move can free up funds while keeping your loved ones safe. Life Insurance Buying Tips for Smart Consumers Choosing the right life insurance means understanding key strategies. By looking at certain factors, we can make better choices. Evaluating Coverage Amount Finding the right coverage amount is key. The DIME formula helps estimate what we need. It considers debts, income, and future education costs. Choosing the Right Type of Policy It’s important to know the different life insurance types. Term life covers you for a set time, while whole life lasts forever

Busting Common Life Insurance Myths Explained

Did you know nearly two-thirds of Americans think they don’t need life insurance? This shows how important it is to know the truth about life insurance. Many people don’t get it because talking about death and money is uncomfortable. We want to clear up these myths so you and your family can make smart choices about protection. We’re going to tackle these common myths and share the facts. Our goal is to give you the knowledge you need to find the right coverage. Knowing the truth about life insurance is the first step to feeling secure and protected. Key Takeaways Many Americans underestimate the necessity of life insurance. Common myths can lead to dangerous misconceptions about coverage. Life insurance provides essential financial security for families. Understanding the facts can motivate informed insurance decisions. Life insurance is not just for those with dependents. It’s important to address misinformation to ensure proper coverage. The Reality Behind Life Insurance Myths Life insurance is more than just a myth. It’s a real deal that helps families when they need it most. It’s a contract where you pay premiums and get a big payout to your loved ones when you pass away. This money can help pay off debts or support your family financially. Understanding Life Insurance Basics It’s important to know the truth about life insurance. Many people think it’s just for emergencies, but it’s also a smart financial move. Learning about how it works and its benefits can help you make better choices. This knowledge helps you pick the right coverage for your family. Why Myths Persist Life insurance myths stick around because talking about death and money is hard. This makes people miss out on its benefits. We need to break these myths and show how life insurance can protect families. By understanding it, we can ensure our loved ones are safe and secure. Busting Common Life Insurance Myths Explained Life insurance is often misunderstood. This is due to myths that can confuse people about its importance. We aim to clear up these myths and show the real value of life insurance. This way, families can be better protected. We will tackle some common misconceptions. These can affect how people make decisions about life insurance. Myth: Life Insurance is Only for the Main Earner This myth ignores the financial help of non-working spouses or caregivers. If a non-working partner dies, families might face unexpected costs. This could include childcare or help with household chores. This shows why life insurance is important for everyone, not just the main earner. It’s about recognizing the value of all family members. Myth: You Don’t Need Life Insurance if You’re Young and Healthy Young and healthy people often think they don’t need life insurance. But life is unpredictable. Accidents or illnesses can happen at any age. Getting life insurance when you’re young can save you money. It also gives you peace of mind. This myth is debunked by showing the benefits of starting early. Myth: Life Insurance is Too Expensive Many think life insurance is too pricey. But there are policies for all budgets. By looking at your needs, you can find affordable coverage. Knowing the real costs can help. It shows that life insurance is worth considering. It’s about finding the right balance for your family’s protection. Addressing Life Insurance Misconceptions Many people have wrong ideas about life insurance. These misconceptions can harm their financial safety. It’s key to know the truth about life insurance to make smart choices. Let’s explore some common myths. Employer-Provided Coverage is Sufficient Some think employer life insurance is enough. But, these policies usually only cover 1-2 times the employee’s salary. This might not cover all financial needs. Also, if you change jobs or lose your job, you could lose your coverage. Life Insurance is Only Necessary if You Own a Home Many believe life insurance is only for homeowners. But, it’s for more than just homes. It helps with debts, future costs, and supporting loved ones, no matter if you own a home or not. Without it, your family could face big financial problems. Life Insurance Payouts Are Always Taxed Some think life insurance payouts are always taxed. But, most of the time, they’re not. Beneficiaries usually get the money without paying taxes. But, there are some cases where taxes might apply. Knowing the facts can help you understand these situations better. Financial Implications of Life Insurance Myths Life insurance myths can affect our financial planning deeply. When people think it’s not needed, they’re not ready for surprises. This can lead to bad choices, leaving loved ones in trouble. How Misconceptions Impact Decision-Making Many skip life insurance because of wrong beliefs about its cost. But, knowing the truth can change things. It’s key to think about our families’ future and make smart choices. The Cost of Waiting to Buy Life Insurance Waiting to buy life insurance can cost more later. As we get older or face health issues, prices go up. Buying early can save money and protect our families. Age Group Average Monthly Premium (Term Life) Impact of Delaying Purchase 25-35 $20 Lower premiums; less financial strain 36-45 $30 Moderate cost increase; possible health risks 46-55 $50 Higher premiums; more financial burden 56+ $100 Big cost increase; fewer options Conclusion We hope this guide has shown why it’s important to clear up life insurance myths. These misconceptions can stop people from making smart choices for their financial future. By debunking these myths, we help people see how life insurance is key to good financial planning. It’s vital to know the truth, whether you’re looking for coverage for yourself or your family. Getting rid of these myths lets you enjoy life insurance’s many benefits. It gives you peace of mind and safeguards your family’s future. When dealing with insurance, always talk to a licensed expert. They can create a plan that fits your specific needs. Being well-informed and taking action is the best way to protect yourself and your

Life Insurance for Parents: Family Future Security

Did you know nearly 60% of American adults lack life insurance? This shows a big gap in financial planning for families. Life insurance for parents is key to securing your family’s future. It offers a safety net, ensuring financial stability in tough times. As parents, we know how vital it is to protect our loved ones. Life insurance helps cover our family’s needs, like living expenses, debts, or education, if we’re not there. This way, we can face our family duties with confidence. To learn more about life insurance options for parents, check out life insurance for parents. Key Takeaways Life insurance serves as a financial safety net for parents. It helps ensure family future security in case of unforeseen events. Investing in life insurance provides peace of mind for families. Coverage can help address major expenses like debts and education. Many Americans remain uninsured, stressing the need for financial protection. Understanding Life Insurance for Parents It’s key for parents to grasp the basics of life insurance for their family’s financial future. Life insurance is a product that pays out a sum to loved ones after the insured person dies. It’s vital for parents to ensure their children and family are cared for after they’re gone. What is Life Insurance? Life insurance is a cornerstone of family financial security. It provides a safety net when a family member dies. The money helps cover daily costs, debts, and unexpected expenses. It’s a financial shield for families. Importance of Life Insurance for Parents Life insurance is essential for parents. It keeps dependents safe financially, even in tough times. It gives parents peace of mind, letting them focus on raising their kids without worry. This insurance also helps fund kids’ education and pay off debts. By valuing life insurance, parents prepare a secure future for their family. Choosing the right coverage offers parents a sense of security. It supports their family and aids in long-term financial planning. Life Insurance for Parents: Protecting Your Family’s Future Life insurance is key to protecting your family’s future and ensuring their financial security. It acts as a safety net for big expenses that might come up when you’re not there. This gives you peace of mind, letting you focus on your loved ones. Financial Security for Your Dependents Life insurance is a great way to help your dependents if you’re not around. It can replace your income and keep their lifestyle going. The right policy covers important costs, like: Daily living costs Childcare and education expenses Outstanding debts and mortgage payments Creating a Safety Net for Major Expenses Life can throw unexpected expenses your way. A good life insurance policy can help manage these big costs. It gives your family a safety net, making it easier to handle tough times. Here are some big expenses insurance can help with: Expense Type Estimated Cost Funeral expenses $7,000 – $12,000 Medical bills $20,000 – $50,000 Child’s college tuition $20,000 – $50,000 per year With the right planning, you can make sure your family is ready for anything. This shows your dedication to protecting their future. Types of Life Insurance Coverage It’s key for parents to know about life insurance types to protect their family’s future. Each type meets different financial needs and goals. We’ll look at term, whole, and universal life insurance. Term Life Insurance Term life insurance covers you for a set time, like 10 to 30 years. It’s cheaper than other types, making it great for families on a budget. It’s best for short-term needs, like paying off a mortgage or college tuition. Whole Life Insurance Whole life insurance covers you forever if you keep paying premiums. It also grows a cash value over time, adding an investment aspect. Families like it for its stability and growth, making it a solid long-term choice. Universal Life Insurance Universal life insurance mixes term and whole life features. It lets you change premiums and death benefits as your life changes. It’s perfect for those who want flexible coverage that can grow with them. Type of Insurance Duration Premiums Cash Value Flexibility Term Life Insurance Temporary (10-30 years) Lower No Limited Whole Life Insurance Lifetime Higher Yes Fixed Universal Life Insurance Lifetime Varies Yes Flexible Choosing the Right Life Insurance Policy Choosing the right life insurance policy is a big decision. It’s important to think about what your family needs. Knowing how much coverage you need helps keep your loved ones financially secure. Looking at different quotes is key. It helps find the best policy for your situation. Assessing Your Family’s Needs When picking a policy, think about a few things: Total annual income Number of dependents relying on that income Outstanding debts, including mortgages and loans Future educational expenses for children Knowing these helps figure out how much coverage your family needs. How Much Coverage is Necessary? Finding the right coverage amount can be tough. Start by adding up basic needs: Annual income replacement (usually for five to ten years) Funeral and burial expenses Existing debts that need to be settled Future financial goals like college tuition This method helps ensure your family is protected financially. Comparing Quotes from Different Providers After figuring out your family’s needs and coverage amount, compare quotes. This step helps see the differences in prices, terms, and benefits. Online tools or a licensed advisor can help. Conclusion Life insurance is key to securing our family’s future. It offers financial support when it’s needed most. It also brings peace of mind, knowing our loved ones are taken care of. Choosing the right life insurance policy is a smart move for parents. It protects our children’s futures, helping them succeed even without us. The right coverage meets our family’s specific needs, securing our future well. We suggest looking into the many options available. Regularly check if your coverage fits your family’s changing needs. If you’re thinking about getting life insurance, start by getting personalized quotes. Look at available life insurance quotes to find the best protection

Determining Your Ideal Life Insurance Coverage

Did you know over 40% of American adults don’t have life insurance? This shows a big gap in being ready for unexpected events. Knowing how to figure out your life insurance needs is key to feeling financially secure for yourself and your family. Life insurance is like a safety net. It helps people, families, and businesses get ready for the unknown. We’ll help you find the right policy and the right amount of life insurance. This way, you can get the best coverage for your needs. Key Takeaways Understanding your life insurance needs is essential for financial security. A significant number of Americans lack adequate life insurance coverage. Life insurance is a vital tool for protecting families and businesses. Evaluating personal circumstances is key in finding the right coverage. Getting the right life insurance amount can ease financial burdens on loved ones. Understanding Life Insurance Basics Exploring life insurance starts with understanding the basics. It serves as a financial safety net for loved ones. It helps protect them from financial troubles after someone passes away. Life insurance is a contract between you and the insurance company. You pay premiums, and if you die, your beneficiaries get a payment. This payment helps cover expenses and debts. What is Life Insurance? Life insurance is a key to financial security. It ensures your loved ones get a death benefit if you pass away. This benefit can help with living costs, loans, and other financial needs. Knowing about life insurance basics is important. It helps you see how it secures your family’s future. Types of Life Insurance: Term vs. Permanent Life insurance comes in two main types: term and permanent. Term life insurance covers you for a set time, like 10 to 30 years. It costs less but doesn’t grow in value. Permanent life insurance lasts your whole life. It can also grow in value over time. Choosing between term and permanent depends on your needs and goals. Importance of Life Insurance for Financial Protection Life insurance is more than just an option; it’s essential for financial planning. It supports your family’s lifestyle and helps settle debts. It ensures your dependents are financially secure. Understanding the need for life insurance is key. It’s a vital part of securing your financial future. It’s a responsible step in planning for the long term. Assessing Your Need for Life Insurance Understanding your need for life insurance starts with knowing your personal and financial situation. It’s important to figure out who needs it. This helps make smart choices about coverage. People with big financial responsibilities should think about how life insurance fits into their plans. Who Needs Life Insurance? Life insurance is vital for many. It helps protect certain groups: Parents: It ensures kids are financially stable if something unexpected happens. Primary earners: It keeps the family’s income safe, protecting their lifestyle. Business owners: It covers business debts and helps with smooth ownership changes. Knowing who needs it shows its value. It brings peace of mind and financial security. Financial Obligations to Consider Life insurance should cover various financial needs: Mortgages: It helps pay off home loans. Student loans: It keeps dependents from inheriting debt. Everyday living expenses: It ensures dependents keep their standard of living. These needs show why life insurance is key. It acts as a safety net for your finances. Evaluating Personal Circumstances Every person’s situation is different. It’s important to consider: Income levels: Those with higher incomes may need more coverage. Overall net worth: Looking at assets and debts helps determine coverage. By carefully evaluating these factors, you can find the right life insurance. For more help, check out our life insurance quote options. How Much Life Insurance Coverage Do You Really Need? Finding out how much life insurance you need can be tough. We can figure it out by looking at different ways to calculate it. It’s important to know our financial needs and goals. Calculating Coverage Based on Debts Looking at our debts is a big part of figuring out life insurance needs. We want to make sure our family isn’t stuck with bills after we’re gone. We should think about: Mortgages Auto loans Credit card debts Personal loans Adding up these debts helps us find a good starting point for coverage. This way, we can rest easy knowing our family won’t struggle financially. Income Replacement Method The income replacement method is another way to figure out life insurance needs. It suggests getting coverage that’s ten times our yearly income. This helps keep our family’s lifestyle going if something unexpected happens. It’s about looking at our current and future earnings. Considering Future Needs: Education and Retirement Thinking about the future is key. We need to consider costs like education and retirement when figuring out life insurance needs. Important things to remember are: Projected education expenses for children Future retirement funding for a spouse or partner Long-term care costs if necessary These factors are big parts of the overall calculation. By planning ahead, we can protect our family’s financial future. Methods to Calculate Your Life Insurance Needs It’s key to know how to figure out life insurance needs to protect our loved ones. There are many ways to get the right coverage for our unique situations and plans. The DIME Method Explained The DIME method is a clear way to figure out life insurance needs. It stands for Debt, Income, Mortgage, and Education. By looking at these areas, we can find the right amount of coverage for our loved ones’ financial safety. Debt: Total outstanding debts, including credit cards and personal loans. Income: Future earnings that dependents would need to keep their lifestyle. Mortgage: The remaining balance on any home loans, ensuring housing security for dependents. Education: Funds needed for future education costs for children or dependents. Standard-of-Living Approach This method looks at how much income is needed to keep a certain lifestyle after we’re gone. It takes into account current expenses, inflation, and future goals. This helps us find the right

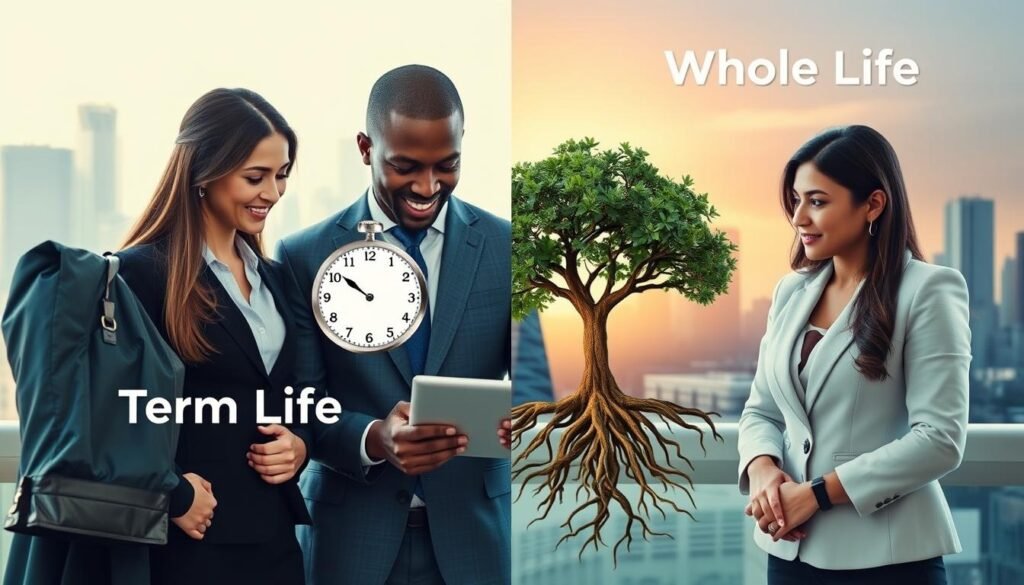

Term Life vs Whole Life Insurance Explained Guide

Did you know about 40% of Americans lack life insurance? This leaves their families at risk during unexpected times. It’s key to know the differences between term life and whole life insurance. In this life insurance guide, we’ll explore these differences to help you make informed choices. We aim to give you the tools to pick the right life insurance for your needs. This will help you feel more secure about your future. Understanding these options can be complex, but we’re here to simplify it for you. Key Takeaways Understanding life insurance is vital for financial security. Term life insurance provides coverage for a specified period. Whole life insurance offers lifelong protection and a cash value component. Cost and benefits differ significantly between the two types. Tailoring your choice to your financial goals is essential. Evaluating your family’s needs can guide your decision-making. Understanding Life Insurance Basics Life insurance is a key financial tool that brings security and peace of mind. It helps individuals and families. By learning the life insurance basics, we can see its role in our lives. Definition of Life Insurance The definition of life insurance is simple. It’s a deal between an insurer and the policyholder. The insurer promises to pay a set amount, called the death benefit, to the policyholder’s loved ones when they pass away. This money helps cover costs like mortgages, education, and living expenses. Importance of Life Insurance Knowing the importance of life insurance is key for planning your finances. It’s a safety net that keeps your finances stable during tough times. It helps families keep their lifestyle, pay off debts, or cover final costs. This gives them peace of mind and security. Exploring this topic can help us make smart choices to protect our loved ones. For more information, check out this resource. What is Term Life Insurance? Term life insurance is a simple way to protect your finances during big life moments. It offers protection for a set number of years, with options for different financial needs. Here’s a quick look at term life insurance, including its key features, flexible terms, and benefits. Overview of Term Life Insurance Term life insurance is for those needing coverage for a short time, usually 10 to 30 years. It’s great for covering needs like raising kids or paying off a big mortgage. This policy is easy to understand and provides the protection you need without being too complicated. Coverage Duration and Options Term life insurance is known for its flexible term lengths. You can choose a term that matches your financial goals. Here are some common terms: 10 years 20 years 30 years If you die during the term, your loved ones get the death benefit. But if you outlive the term, the coverage ends and no money is paid out. This clear structure helps everyone understand what to expect. Term Life Insurance Benefits One big plus of term life insurance is how affordable it is. Its premiums are often lower than those of whole life insurance. This makes it a good choice for many looking for financial security without breaking the bank. Some main benefits include: Lower premiums compared to permanent life insurance. Flexibility in choosing coverage duration based on individual needs. Simplicity that allows for easy understanding of policy terms. In short, term life insurance gives you peace of mind. It ensures your loved ones are financially secure if something unexpected happens. What is Whole Life Insurance? Whole life insurance offers lifelong protection. It’s different from term policies because it has fixed premiums and a cash value. This makes it appealing for its death benefit and chance to grow your money. Overview of Whole Life Insurance This policy covers you for your whole life if you keep paying premiums. It’s known for its stable costs and guaranteed death benefit. It’s a good choice for those wanting to leave a lasting financial mark. Key Features of Whole Life Insurance Lifelong Coverage: Protection lasts for the entire life of the insured. Fixed Premiums: Premium costs remain constant, making budgeting easier. Guaranteed Death Benefits: Beneficiaries get a set amount when you pass away. Potential for Dividends: You might get dividends from the insurer’s success, adding value. Whole Life Insurance Cash Value The cash value part of whole life insurance is key. It grows over time and can be used when needed. This growth is tax-free, making it attractive for financial planning. Term Life vs Whole Life Insurance Explained Choosing between term and whole life insurance requires understanding the key differences. These policies vary in coverage length, cost, and purpose. We’ll explore how these differences affect your financial planning. Primary Differences Between Term and Whole Life The primary differences between term and whole life insurance are clear. Term life covers you for a set time, like 10 to 30 years. It’s great for meeting short-term needs, like raising kids or paying off a mortgage. Whole life, by contrast, covers you for life. This is key for those seeking long-term security. Cost Comparison Looking at the cost comparison term life and whole life insurance shows term life is cheaper. Term life premiums are much lower than whole life. Here’s a comparison: Insurance Type Typical Monthly Premium (Age 30) Coverage Duration Total Benefit Term Life Insurance $25 10-30 years $500,000 Whole Life Insurance $200 Lifetime $500,000 Who Should Consider Each Option? People with different financial needs might prefer one over the other. Term life is perfect for young families or those needing short-term protection. Whole life is better for long-term planning and leaving a legacy. Pros and Cons of Term Life Insurance When thinking about term life insurance, it’s key to look at both sides. This helps people make smart choices that affect their families and future. The good and bad points of term life insurance depend a lot on your personal situation and goals. Advantages of Choosing Term Life Term life insurance is often cheaper than other types. This makes it a good choice for

Safeguarding Your Future: Why Life Insurance Is Key

Did you know nearly 70% of Americans think life insurance is key for financial planning? Yet, many don’t have enough coverage. This shows a big gap in understanding life insurance’s role. Knowing why life insurance is important is vital to keep our loved ones financially safe. Life insurance is more than just protection. It’s a cornerstone for financial security. It helps us feel secure in uncertain times. By getting life insurance, we protect our families from unexpected costs and bring peace of mind. Key Takeaways Life insurance plays a vital role in safeguarding financial security. A significant number of Americans recognize its importance yet remain underinsured. Securing life insurance provides peace of mind for individuals and families. Understanding coverage options is essential for informed financial planning. Life insurance can serve as a protective measure during times of financial stress. Proper planning ensures stability and security for future generations. Understanding the Importance of Life Insurance Life insurance is key to financial planning. It ensures financial security and peace of mind for families. It’s a safety net against life’s surprises. Many people worry about their finances, fearing how unexpected events could affect their loved ones. Life insurance helps ease these concerns. Financial Security and Peace of Mind Life insurance is vital. It keeps families financially stable even when faced with tough times. Studies show that many families struggle to keep up without their main breadwinner. Life insurance protects families from financial stress. It lets them focus on healing, not worrying about money. Life Insurance as a Safety Net Life insurance is more than just money. It reassures families they won’t be overwhelmed by financial problems. It gives them peace of mind. This peace of mind lets people live without constant worry. Life insurance is a shield against financial stress in critical moments. Why Life Insurance Is a Key Part of Financial Planning Adding life insurance to your financial plan is key for long-term stability and peace of mind. It helps you understand your financial needs and tackle debt. This creates a strong base for security when things get tough. Evaluating Your Financial Needs It’s important to figure out how much coverage you need to support your family. Life insurance should be 7 to 10 times your annual income. This way, your family can keep going even if you’re not there. Addressing Debt and Final Expenses Life insurance also helps with debt. It can pay off what you owe, easing the burden on your family. Don’t forget to think about final expenses like funeral costs. This way, you protect your loved ones from financial worries, ensuring a secure future. Types of Life Insurance: Making an Informed Choice Understanding the different types of life insurance is key to making smart choices. There are mainly two types: term life insurance and permanent life insurance. Each has its own benefits, fitting various financial needs and goals. Term Life Insurance Term life insurance covers you for a set time, usually 10 to 30 years. It’s often cheaper than permanent life insurance. This makes it great for those with tight budgets. It helps protect loved ones during important times, like raising kids or paying off a mortgage. Permanent Life Insurance Permanent life insurance lasts your whole life and grows a cash value. It costs more, but offers more than just basic coverage. You can even borrow against the cash value. It’s perfect for long-term planning, like securing your family’s future or estate planning. Examining Life Insurance Coverage Levels It’s key to know how much life insurance you need to protect your family’s money. Many don’t realize how much they need, which can lead to not having enough. By looking at your situation closely, we can make sure your family has the money they need when they need it. Calculating Coverage Requirements To figure out how much coverage you need, you have to look at your finances. Important things to think about are: Existing debts, including mortgages and personal loans Your annual income and what you might earn in the future Future costs like education for your kids Final costs like funerals and medical bills This helps us find out how much life insurance you need to keep your family safe. A plan made just for you makes sure all your bills are paid and you won’t be underinsured. Considerations for Underinsurance Many people and families face the problem of underinsurance. This happens when your life insurance isn’t enough to cover your financial needs after a loss. To avoid this, you need to check your policy often as your life changes. Things to watch are: Changes in income or job status More family members or dependents More debts and financial responsibilities Keeping an eye on these things helps prevent gaps in coverage. This way, you can have peace of mind knowing your life insurance covers your needs. Life Insurance in Future Planning: A Smart Strategy Adding life insurance to our future plans is key for protecting wealth and facing financial risks. The right policy creates a safe financial cushion for our loved ones. It also keeps our wealth safe over time. Life insurance is a smart choice for both growing and protecting our wealth. Using Life Insurance for Wealth Protection Wealth protection means keeping our financial legacy safe from unexpected events. Life insurance is a vital part of this plan. Some policies grow in value, boosting our finances while preparing for the future. This way, we can rest easy knowing our assets are safe for our family’s future. Mitigating Financial Risks with Insurance Life’s surprises can hit hard financially. Using life insurance in our future plans helps manage these risks. It ensures funds are ready for our loved ones, helping them with debts and other costs. This planning keeps our financial dreams alive, even in tough times. Conclusion Life insurance is key as we face life’s challenges. It helps protect our future and gives us peace of mind. It’s a vital part of our financial planning, making sure